See the direction of business spend

Coupa + MIT Data Science Lab move beyond sentiment surveys.

Get the BSI Report

Predicting the future of business spend, faster

Coupa + MIT Data Science Lab move beyond sentiment

COUPA + MIT DATA SCIENCE LAB BUSINESS SPEND INDEX REPORT 2026 EDITION

The Coupa + MIT Data Science Lab Business Spend Index (BSI) Report turns real business spend into a clear signal of economic momentum. Skip sentiment surveys and lagging indicators and get deep sector analysis, near-term forecasts, and proven spend trends driven by business conditions.

Download Executive Summary Learn More

Section 1

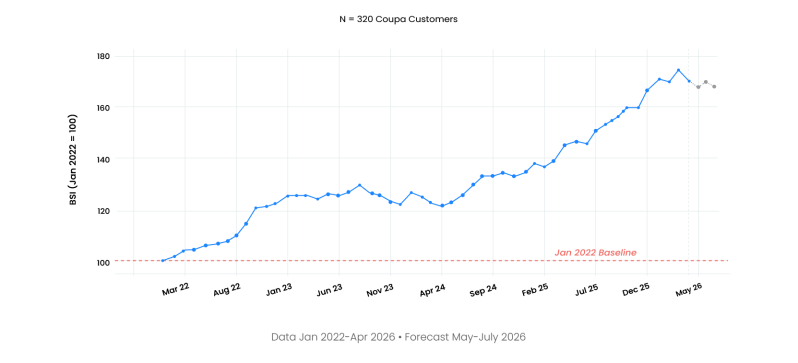

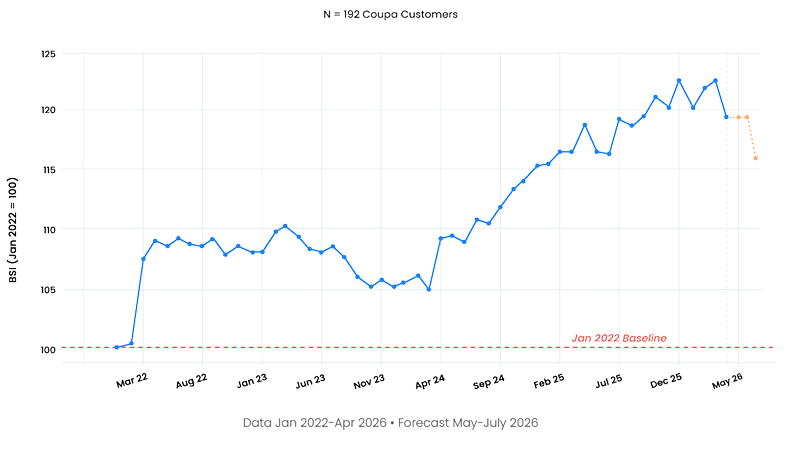

High Technology:

Accelerating with potential for moderation

High Technology is entering an investment-led expansion, with spend accelerating to new highs as companies fund AI projects, modernize core systems, and strengthen controls. This upward momentum has been building since mid-2024, and shows no sign of plateauing, with the BSI reaching its highest level in the four-year series.

It is worth noting that the BSI captures primarily indirect procurement in categories such as software, services, and consulting versus the infrastructure layer of compute, hardware, and data centers. It gives a window on the demand-side growth, which is useful because enormous capital has been deployed on AI infrastructure predicated on the assumption that enterprise demand will follow. The High Technology BSI offers an early signal on whether that bet is paying off.

Download the full BSI Report to learn how to change your business for the future

Download Now

Section 2

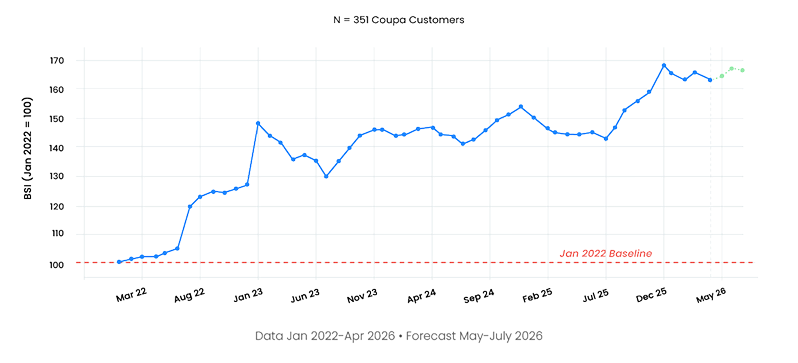

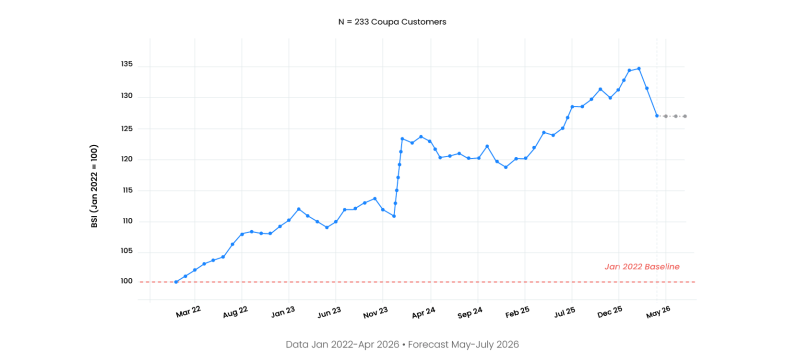

Manufacturing:

Bold investments alongside caution about soft demand

Manufacturing spend has surged to new highs, but the path there tells a more specific story than a simple late-cycle investment narrative. The BSI observes three distinct phases, each tied to the evolving tariff policy environment rather than underlying demand.

In late 2024, Manufacturing procurement accelerated following the U.S. presidential election, consistent with manufacturers anticipating incoming trade policy and pulling forward purchases before input costs rose. Tariffs then began landing in early 2025. Our joint analysis with MIT Data Science Lab shows that between February and May 2025, invoice approval times fell 26% relative to 2023-2024 baselines, even as procurement spend declined 16% compared to year-over-year historical trends. Firms moved faster on the purchases they did make, but bought less overall.

On the BSI chart, this contraction appears as a flattening and modest decline rather than the sharp drop the MIT Data Science Lab data reveals. This is by design: The BSI applies seasonal adjustment and a three-month exponential moving average to emphasize persistent trends, which smooths short-duration shocks. The MIT Data Science Lab analysis, working from unadjusted transaction-level data over a specific window, captures dynamics that the BSI's methodology is built to absorb. The two views are complementary: The BSI shows where the trend is heading; the granular data shows what is happening in the moment.

Section 3

Financial Services:

Holding steady at an elevated baseline

Financial Services tells a different story than the other growth sectors in the BSI. While High Technology and Manufacturing surged on AI investment and tariff-driven restructuring, Financial Services traced a narrower band, climbing gradually over four years with little volatility. The sector grew, but it did not accelerate with the AI-era investment cycle that lifted its peers.

That AI-driven acceleration pattern is not visible in Financial Services at the aggregate level, which covers compliance, technology, cybersecurity, operations, consulting, and more. Those components may be moving in different directions in ways that offset at the aggregate level. For example, a deregulation-driven easing of compliance spend could be offsetting a cybersecurity increase. A defensive AI posture could coexist with slower adoption of AI in core business functions. Future editions of the BSI will dig in deeper.

Section 4

Business Services:

Elevated and embedded

Transformation pressure is hitting every sector simultaneously: AI adoption, supply chain restructuring, regulatory compliance, cybersecurity, and cloud migration. These demands exceed what any organization's permanent workforce was sized to deliver. Companies cannot hire full-time employees to respond, so they buy that capacity externally: integrators, consultants, managed service providers, contingent labor, compliance specialists, and so on.

The pace of change isn't slowing, so what used to be project-based consulting is becoming a permanent operating mode and is driving Business Services supply to meet demand.

The assumption is that external services are now an embedded part of simply running the business. We will watch closely over the next 12 months to see if this represents a more permanent, structural change.

Section 5

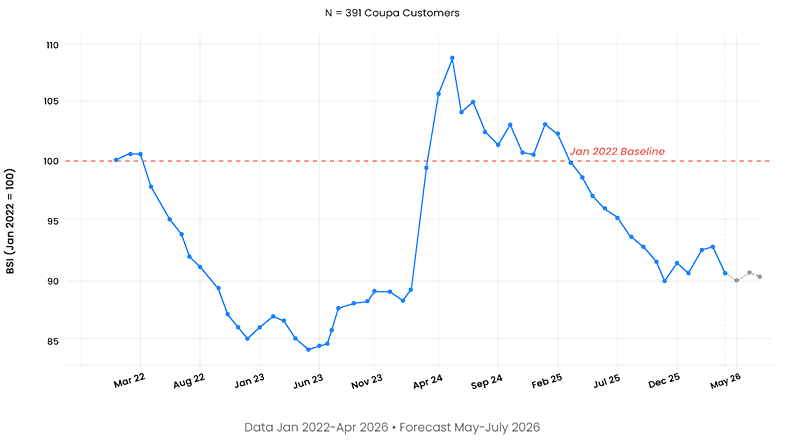

Healthcare & Life Sciences:

Contracting with no catalyst for recovery

Healthcare & Life Sciences is the outlier in the BSI. Every other sector is well above its January 2022 baseline while this sector is in decline.

Because the BSI combines providers and life sciences into a single cohort, the aggregate index may understate the severity of both contractions. A provider-only BSI might show steeper decline; a life sciences-only BSI might reveal a sharper, more recent drop concentrated in 2025 as grant disruptions took hold. We’ll be taking a closer look at this sector in the next edition.

Find out what $10 trillion in community data has to say.

Oh! It looks like you opted out from using the needed cookies. If you are interested in using the AI Agent, then please opt-in to the cookies in the preference center.

Update preferences